1. Why Make a Budget?

Creating a monthly or annual budget may seem like an overwhelming task, especially if you've never tried to do one in the past. Most people have money being used for a huge variety of purposes every month, and amounts spent often vary from one month to the next. This is completely normal, and in fact, virtually everyone who creates a budget deals with the same issue.

While it might initially seem overwhelming, making a budget is something that will eventually make your life much easier.

A budget gives you—and in fact your entire family—a simple way to discuss money. It can be an excellent teaching tool for your children, and it can help reduce stress regarding money. Instead of wondering whether you can afford something, you will already know.

With a budget in place, you'll be much better equipped to resist those impulse purchases that can wreak such havoc on your finances.

The information in this book is organized in such a way that making a budget will not only be easy, but it will actually make sense while you're doing it. The goal of this e-book is to give you a clear picture of your current finances, help you create a workable plan to pay your bills reliably and on time, and a plan for the big events and unknown expenditures you will face in the future. You'll be able to prepare for emergency situations, which will ensure that one emergency doesn't cripple you financially.

As you read through this e-book, try to keep your current income in mind, as opposed to your future or desired income. This helps ensure that you're setting realistic budgeting goals. Take as much time as you need to read through the following information. Your wallet (and your bank account) will thank you for it!

2. Putting Your Expenses to Paper

This first step may be the hardest, but once you've put your expenses to paper, you'll be in great shape for budget creation. As you work on this category, keep a few things in mind.

• If you don't have exact figures for a category, estimate as closely as possible. Round up when in question so you give yourself some wiggle room, but don’t underestimate a significant expenditure.

• For expenses that you pay only once a year, divide by 12 to get a monthly figure. For weekly expenses, multiply by four to get a monthly cost.

• Some of the categories below include non-recurring expenses that may seem too small or insignificant to note; but don't fall into this trap. A number of those smaller non-recurring expenses could happen at once, causing a large sudden dent in your bank account if you don't plan for them. Divide those costs by 12 to get a monthly average, but make a note that it's a non-recurring expense while completing the table to avoid confusion as you add the figures.

Use the following categories as a guide while writing down your expenses. Record your answers in the blanks provided or in an excel spreadsheet, if that is a program you would prefer to use.

Once you have monthly figures for each of these, add everything up to get a good general idea of how much you're spending every month. It may be more than you had realized—don't worry, the next steps will help you correct that. Be sure to keep the figure reflecting your total monthly expenditures close at hand, you'll need it in the coming exercises.

3. Setting Realistic Goals

Expert financial strategists always say that the number one way to stick to a budget is to keep your goals in sight. Everybody has their own financial goals, so take this time to think about what you'd like to do with your money, both for the short-term and for the long-term.

Maybe you dream of being debt free, or maybe you have a certain retirement savings goal that you'd love to meet. Perhaps you want to fund your child's college education, or pay for a year-long sabbatical in Europe.

The more specific you are with the following list, the better your chances of achieving it. Think about what truly motivates you. What do you want the most out of life? Include those goals in your budget. Some people create goal inspiration mood boards with images to keep them focused on the prize they are working toward.

The Short-Term Goals

First, write down at least a few short-term goals, the goals you'd like to achieve within six months. These goals should be very specific, with exact dollar amounts attached. Maybe you want to:

- Pay off a credit card

- Purchase a new big-screen television

- Pay for a short vacation

- Purchase a special piece of artwork or other collectible

The Intermediate Goals

The intermediate goals are financial goals that you can likely achieve in more than six months, but less than five years. These goals may be fairly large ones, but remember that you'll have anywhere from six months to five years to achieve them.

The intermediate goals should be as specific as possible in terms of cost, but they don't have to be as exact as the short-term goals. Consider things like:

- Save a down-payment for a new vehicle

- Pay for an elective surgical procedure that your insurance won't cover

- Pay for a small kitchen or bathroom renovation for your home

- Buy a CD, which will allow your money to make money for you

- Purchase new living room furniture

- Pay for a week-long vacation somewhere special

The "Half-Decade" Goals

The half-decade goals are those that you'd like to achieve in the next five to ten years or so. These goals can be a bit less specific. Just estimate these goals as closely as you can.

The half-decade goals may include things like:

- Pay for a major family trip to Europe or other far off destination

- Add a bedroom (or even a bedroom suite) to your home

- Create a 12-month emergency fund

- Purchase a new vehicle in cash

- Save an additional large sum of money for retirement

The Ultimate Goals

The ultimate goals are the long-term goals, the ones that are your lifetime dreams. The costs of this goal need not be exact, but try to estimate if it's possible. The ultimate goals could be things like:

- Buy a vacation home

- Pay for your children to go to college

- Purchase a property where you can build your dream home from scratch

- Launch your own business, for example, open a restaurant

- Open an animal sanctuary

4. Making Your Goals a Reality

With the goals firmly in mind, you can now start creating a way to meet them. Begin with one of your smaller short-term goals. Now, all you have to do is write down the dollar amount that you assigned to the goal and divide it by six. Remember, this goal will be achieved in six months.

Once you have that figure, you know what you need to do: Come up with that amount every month. If you don't have the extra money, you just have to get creative.

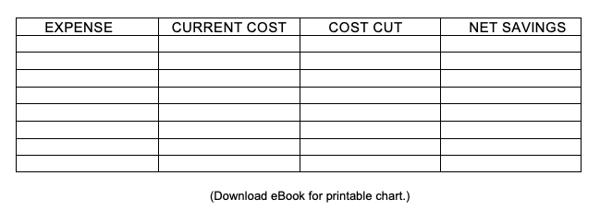

Start looking for ways to cut the fat from the expenses that you've already documented. While you may not find a way to take all the money you need from one category, it’s likely that you can find several different areas to cut back in at once. PRO TIP: You might want to look at your "fun stuff" category to start.

Maybe you're spending $150 each month on somewhat over-priced coffees at Starbucks. You could make that coffee and dress it up at home for a tenth of the cost – just $15!! This cost cut nets you $135 towards your goal.

If you're currently paying $100 a month for cable, consider whether you really need all those channels. Can you cut back to basic cable to save another $50 per month? Look closely at how much you're spending on dining out, too.

Even skipping one meal out per week could save you an easy $100 per month, maybe more.

Add up all of your net savings to find out how much you can be putting towards your goals. These are generally very easy changes to make, but the benefits are huge.

Consider using an online financial calculator to make the financial goal planning even easier. By creating and achieving these short-term goals, you'll see that managing your money better really is possible. As you achieve each goal, you can choose whether to move on to a new goal or to go back to your old spending habits.

But what people often realize and are surprised to learn is that they don't really miss the old way of living paycheck to paycheck, and you definitely won't miss wasting money when you finally achieve one of the fun goals you’ve worked hard for!